Why a Customer-Centric Banking Model is Essential

Ten Questions to Ask When Choosing a CRM in Banking

Download our infographic for 10 must-ask questions to help guide you in your evaluation of your next CRM platform.

Download the InfographicGiven the proliferation of banking technology and the industry-wide emphasis on digital transformation, it might seem strange to hear that it’s more important now than ever before for banks to return to basics — but let’s take a moment to think about what that really means. What is the one thing that is absolutely vital to the continued success of any financial institution, the one thing that guarantees consistent, repeat business?

Happy customers.

With customer expectations at an all-time high, and fintech firms waiting in the wings to stake their claim on market share, it’s imperative that banks rededicate themselves to understanding their customers on an intuitive level and delighting them at every opportunity. Although technology can help you achieve these goals, without a solid customer-centric strategy to act on, it’s little more than expensive window dressing.

Create a Customer-Centric Banking Model With Big Data

Customer-centricity isn’t as simple as asking customers what they want and making good on it, though that’s certainly part of it. Customer-centricity requires banks to re-evaluate what they know about their customers and to better understand who their customers are, what interests them, what they value, and what drives them. It’s about building a relationship that is more meaningful than the transactional one banks traditionally have with their customers — a relationship that looks more like a partnership and that is attuned to the customer’s needs.

Data lies at the heart of this type of relationship. Financial institutions collect massive quantities of data throughout the various stages of the customer journey — the sales cycle, onboarding, customer service inquiries, and so on — across multiple channels, as well as through data aggregation from third-party resources. This data, despite having infinite potential, is of little use if it isn’t consistently processed and analyzed. The natural first step of any customer-centric approach in banking is to segment customers by demographic and then segment at an even more granular level by building out detailed individual customer profiles. These end-to-end customer profiles should include the following information:

To demonstrate why customer profiles matter, let’s look at a few examples:

- For “Attitudes,” you might ask a customer whether they’re confident about financial matters. If their answer is “No,” that customer could potentially be a good candidate for financial advising services.

- For “Personal Preferences,” you might ask a customer whether they prefer to handle customer service inquiries on their own, or if they appreciate a helping hand. If they prefer the former, you might recommend that they use your mobile banking application for self-service.

- For “Milestones,” if your customer indicates that they were recently married, it might make sense to target them with a personalized marketing campaign offering low interest home loans.

You’ll notice that, in each of these examples, the customer’s preferences, values, and interests are treated as a top priority, and your bank is positioned to engage accordingly. That’s because a true customer-centric banking model not only helps financial institutions gain a 360-degree view of the customer and uncover valuable insights, it also represents a commitment to making customers feel as though their bank truly understands what they want and need.

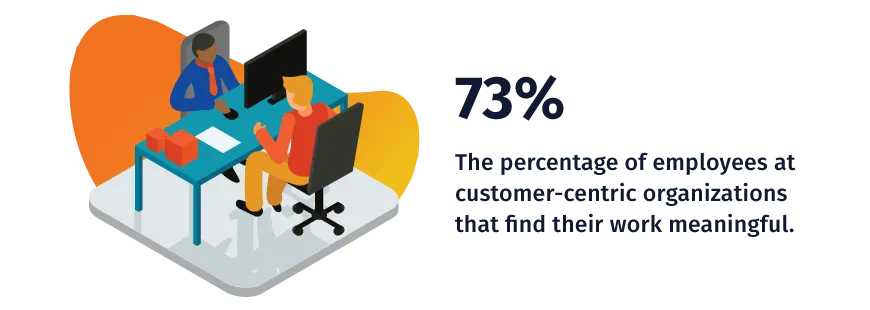

Now that we’ve covered the basics of customer segmentation in banking, let’s take a minute to talk technology — after all, customer profiles don’t just build themselves. A customer relationship management (CRM) system gives banks a centralized database in which they can store customer data and develop customer profiles. By granting your employees access to this repository, you enable them to regularly update profiles with new information after each interaction and to use the information contained within a customer’s profile to provide more personalized service. Figures show that adding this kind of human touch to the customer experience benefits customers and employees alike: Among employees who report that customer-centricity is a key priority within their organization, 73% find their work meaningful.

Be Proactive With Predictive Analytics

Another way to pair strategy and technology for greater customer-centricity in banking is with predictive analytics. When accumulated over time, the data within a CRM system can be used to identify behavioral patterns and build predictive models that reveal valuable customer insights or operational inefficiencies. For example, if a customer has a documented history of visiting branch locations in person, they’re likely to do so again in the future. Although this is a relatively simplistic example of predictive analytics in action, it gets the basic point across.

For a more complex understanding of how predictive analytics can help you develop a more customer-centric approach in banking, let’s say you want to proactively look for ways to optimize how your call center handles customer inquiries. After analyzing call history data sets across different customer demographics — for example, Baby Boomers, Gen X, Millennial, and Gen Z — you notice two distinct behavioral patterns:

- That customers frequently call in with simple questions, such as how to send a wire transfer or what types of transactions are covered by overdraft protection

- That call center wait times average between 20–30 minutes

Based on your findings, you kickstart an initiative to build an online customer resource center; this resource center includes a knowledge base and an AI-enabled chatbot, both of which customers can refer to for basic inquiries and problem resolution. This initiative ensures that only complex service requests are funneled to the call center, which reduces call volume and wait times and improves customer satisfaction. As you can see from this example, you can use predictive analytics to proactively look for and resolve process inefficiencies that could negatively impact the customer experience.

Another way you can use predictive analytics to create a more customer-centric banking model is to deliver product and service offerings tailored to the customer’s specific needs and interests. For example, if a customer held a balance of over $10,000 in their savings account, you might proactively offer them a high initial rate CD the next time they log in and suggest that they work with an in-house financial advisor to see how much they could earn in higher interest. Or, if a customer’s transaction history indicates that they’re a frequent flier but your records also show that they don’t have your bank’s travel rewards card, you might send them a targeted travel rewards program marketing campaign.

In this way, predictive analytics not only presents your institution with valuable upselling and cross-selling opportunities — it also allows for greater customer-centricity because it makes customers feel as though you’ve accurately anticipated their needs.

Reward Customer Loyalty With Exciting Incentives

Once you’ve discovered the secret to creating happy customers, the next step in your customer-centric strategy is to figure out how to keep them. You’ve likely heard the statement that it’s more expensive to acquire a new customer than to retain an existing one, but are you aware of how much? According to research from Customer Think, it costs banks approximately $200 to acquire a new customer; the typical banking customer, on the other hand, generates approximately $150 in revenue each year, meaning it can take up to two years to turn a profit from a new customer.

Based on these numbers, it’s imperative that banks earn and reward customer loyalty with exciting incentives. A travel rewards program — like the one mentioned earlier — that enables customers to earn credit card miles with every purchase is just one way to show appreciation for your customers. For some other examples of customer loyalty rewards programs in action, consider the following:

- With Citibank’s ThankYou rewards program, customers earn points either by making purchases with a Citi credit card or by linking their Citi checking account to qualifying products or services. Customers can then redeem these points to purchase gift cards, book flights, make charitable donations, pay bills, and so on; ThankYou members can even transfer their points to participating loyalty programs or share them with other ThankYou members.

- Bank of America’s (BoA) Preferred Rewards offers tier-based rewards based on a customer’s qualifying combined balances in their BoA banking and Merrill investment accounts. For example, customers with a qualifying balance of $50k–$99.3k are eligible for the Platinum Tier, which comes with a 10% savings interest rate booster, a 50% rewards bonus on eligible credit cards, a $400 reduction in mortgage origination fees, and more.

- Similar to Citibank, Wells Fargo’s Go Far Rewards program enables customers to sign up for a rewards-based credit card, which they can use to rack up points that can be redeemed for gift cards, retail items, travel expenses, charitable donations, and more.

When developing your own banking loyalty rewards program, it’s important to keep it simple — customers are put off by programs that are needlessly complex or have a lot of fine print. Customer-centricity favors simplicity, so the easier it is for your customers to earn points (or whatever value system you choose to implement), the more likely they are to participate in your program. Use data-driven analytics to determine what types of incentives will appeal to your customer base — for example, credit unions might want to partner with local businesses rather than major retailers to develop incentives that support the community. Finally, develop a user-friendly portal that makes it easy for your customers to keep track of and redeem the points they’ve accrued.

Discover the Keys to Customer-Centricity in Banking

We’ve covered a lot of ground in this article, and yet we’ve only just scratched the surface — these tips will serve you well when developing a customer-centric approach in banking, but partnering with a dedicated consulting team will take you even further.

At Hitachi Solutions, we specialize in working with banks to drive customer retention and fuel growth. We offer an entire suite of products and services built on the Microsoft platform and designed specifically for financial institutions seeking to empower employees, optimize operations, and engage customers. To find out how Hitachi Solutions can help you take advantage of the customer-centric banking model, contact us today.